August 24, 2013

Tax season has a way of reminding real estate investors exactly how much they don't have organized. You know the rent came in. You know you paid for repairs, insurance, and a property manager. But pulling it all together — property by property, category by category, in the exact format the IRS requires — is where things get messy.

That form is Schedule E. It's not complicated once you understand how it works. This guide walks through how Schedule E works, what goes on each line, how to track income across multiple properties without losing your mind, and what the rules actually mean for investors who hold properties in multiple LLCs.

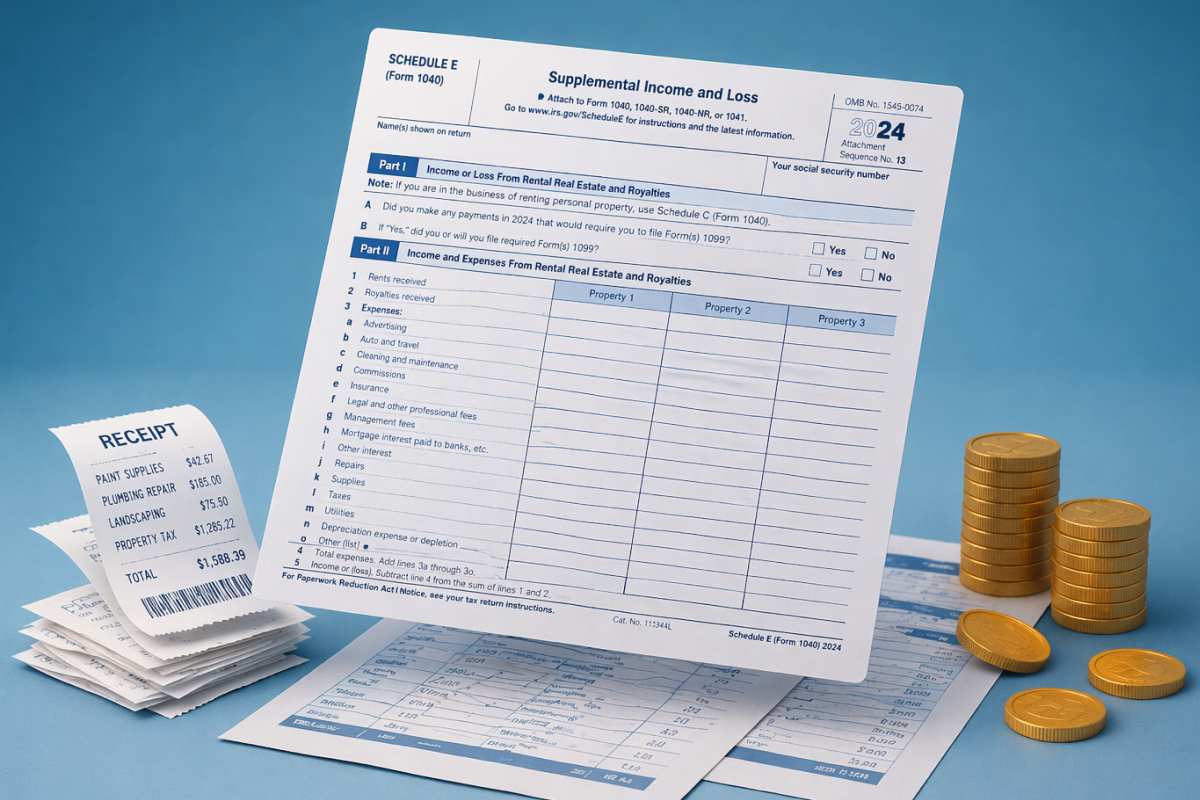

Schedule E (Form 1040) is the IRS form for reporting supplemental income and loss, including rental real estate. It covers income or loss from rental real estate, royalties, partnerships, S corporations, estates, and trusts. For most rental property owners, Part I is the one that matters — that's where you report each property's income and expenses.

If you collect rent from a property you own and you're not in the business of providing significant services to tenants, you almost certainly file Schedule E. It doesn't matter whether you own the property personally, through a single-member LLC, or through a partnership — the income ends up on Schedule E one way or another, though the path there differs.

One thing Schedule E is not: a business income form. Rental income is passive income under the IRS's classification, which means it isn't subject to self-employment tax. You won't pay Social Security or Medicare tax on your rental profits. That's one of the genuine advantages of real estate over other income-producing activities.

Schedule E is for passive rental income — income from properties you own and rent, but don't run as an active business. The IRS doesn't consider most landlords self-employed, so rental profits aren't subject to the 15.3% self-employment tax.

Schedule E Part I holds up to three rental properties per page. If you own more than three, you attach additional copies. Per the IRS Schedule E instructions, each property must be listed separately — you can't combine income and expenses across properties into a single line. The combined totals only flow to lines 23a–26 on one designated copy.

The reason is simple: the IRS applies depreciation, passive activity rules, and income thresholds at the property level. Lumping properties together would make it impossible to track which losses belong to which asset, especially when you sell one property and need to release suspended passive losses tied specifically to it.

For investors with multiple properties, this means your accounting system needs to track transactions at the property level, not just at the account level. If you're running three properties through one bank account and categorizing everything together, you're going to spend a weekend reverse-engineering your own finances before you can fill out a Schedule E. (Or paying your CPA to do it.)

That's a core reason investors move to dedicated real estate accounting software. When every transaction is tagged to a specific property from the moment it hits your account, the Schedule E numbers are already organized. You're pulling a report, not building a spreadsheet.

Lines 5 through 19 of Schedule E are where you report deductible expenses for each rental property. Getting these right matters, not just for accuracy, but because misclassifying a capital improvement as a repair is one of the most common audit triggers for landlords.

Line 14 — Repairs — is where a lot of investors make expensive mistakes. The IRS distinguishes between repairs and improvements. A repair maintains the property in its current condition and is deductible in full in the year you pay it. An improvement adds value or extends the property's useful life and must be capitalized and depreciated over time.

The cost doesn't determine which category it falls into. A $4,000 repair is still a repair. A $400 improvement is still an improvement. When in doubt, ask your CPA — getting this wrong in either direction costs money.

Depreciation — line 18 — is usually the largest single deduction on a rental property's Schedule E, and it's one most investors underutilize. IRS Publication 527 allows you to deduct the cost of a residential rental building over 27.5 years using MACRS (Modified Accelerated Cost Recovery System). That works out to roughly 3.636% of the building's depreciable value per year.

Here's the key detail: only the building depreciates, not the land. You need to separate your purchase price into land value and building value — typically done using your property tax assessment as a guide. If your tax bill says land is 20% of assessed value, then 80% of your purchase price is your depreciable basis.

Example: You buy a rental house for $350,000. The county assessment values land at $70,000 and the structure at $280,000. Your annual depreciation deduction is $280,000 ÷ 27.5 = $10,182 per year.

That $10,182 is a non-cash deduction — you didn't write a check for it, but it reduces your taxable rental income dollar for dollar every year. On a property generating $24,000 in gross rent, depreciation alone might eliminate most or all of your taxable income even in a profitable year.

Two things most investors learn the hard way. First, depreciation must be claimed or it's still recaptured when you sell. The IRS recaptures depreciation you were allowed to take even if you didn't take it, at a rate up to 25%. Skipping depreciation doesn't protect you from recapture — it just costs you the deduction. Second, depreciation starts when the property is placed in service — meaning available to rent, not when a tenant actually moves in.

Schedule E rental income is passive income. That's good news for taxes because it avoids self-employment tax. But it comes with a trade-off: rental losses are generally passive losses, which means they can only offset passive income — not your W-2 wages or active business income.

There's an important exception. If your modified adjusted gross income (MAGI) is $100,000 or less and you actively participate in managing your rental properties, the IRS allows you to deduct up to $25,000 of rental losses against other income each year. Active participation is a relatively low bar — it means you make management decisions like approving tenants, setting rents, and authorizing repairs. You can hire a property manager and still qualify.

According to IRS Publication 925, this $25,000 allowance phases out between $100,000 and $150,000 of MAGI. For every $2 your income exceeds $100,000, the allowance drops by $1. At $150,000, it disappears entirely.

MAGI under $100,000: Full $25,000 allowance available. MAGI $100,000–$150,000: Allowance reduced by $1 per $2 over $100,000. MAGI $150,000+: No allowance — losses suspended and carried forward.

Example: MAGI of $130,000 → ($130,000 – $100,000) ÷ 2 = $15,000 reduction. Allowance drops to $10,000.

Losses that exceed your allowance don't disappear — they're suspended on Form 8582 and carried forward indefinitely. They'll offset future rental income, or they're released in full when you sell the property in a fully taxable transaction. Years of suspended losses can offset a large gain when you eventually sell, which is a meaningful benefit for long-term portfolio builders.

Here's what changes when you have multiple properties: the passive activity rules apply to the aggregate. If Property A generates $8,000 in profit and Property B generates $15,000 in losses, your net rental loss is $7,000 — and that's what goes through the passive loss analysis. You don't analyze each property in isolation.

This is also why tracking income and expenses per property matters for more than tax prep. Understanding which specific properties are generating losses — and why — is how you make decisions about what to hold, what to improve, and what to sell.

This is where things get more complicated, and where most accounting tools start to show their limits.

A single-member LLC that owns rental property is a disregarded entity for federal tax purposes. The LLC doesn't file its own tax return — you report the income and expenses directly on your personal Schedule E, just as if you owned the property personally. From the IRS's perspective, a single-member LLC is invisible. You still need to track each property's finances separately, but it all flows to your Schedule E.

A multi-member LLC — one with two or more owners — is treated as a partnership by default. The LLC files a Form 1065 partnership return and issues Schedule K-1s to each partner. Partners then report that K-1 income on Part II of their Schedule E, not Part I. This is a different process, with different forms and a different set of rules.

What this means practically: if you have five LLCs and three of them are single-member, two are multi-member partnerships, you're dealing with both Part I and Part II of Schedule E — plus two Form 1065s — plus K-1s. Kestrel's multi-entity management is built specifically for this structure, keeping each entity's books clean so the right numbers flow to the right forms at year end without manual reconciliation.

Single-member LLC → disregarded entity → income reports directly on your Schedule E Part I. Multi-member LLC → treated as partnership → files Form 1065, issues K-1 → you report K-1 income on Schedule E Part II.

The answer to a clean Schedule E isn't what you do in March. It's what you do every month. Investors who have a smooth tax season are usually doing three things consistently:

Per the IRS's rental property recordkeeping guidance, good records are required to monitor property performance, prepare financial statements, identify receipt sources, and support items reported on your return. The burden of proof sits with you, not the IRS.

For investors with one or two properties, a dedicated spreadsheet can work if you're disciplined. For investors with three or more properties — especially across multiple entities — the tracking complexity justifies dedicated software. Not because the spreadsheet can't hold the data, but because the discipline required to maintain it accurately doesn't scale.

Do I need a separate Schedule E for each property? Not exactly. Each Schedule E page holds up to three properties. If you own four or more, you attach additional pages. One page serves as the "master" that carries the combined totals.

What if my rental shows a loss every year? Common, especially in early years when mortgage interest and depreciation are highest. Whether you can use that loss against other income depends on your MAGI and active participation status. If not, the loss suspends and carries forward — it's not wasted.

Can I deduct a home office I use to manage my rentals? Potentially, but carefully. The space must be used exclusively and regularly for rental management. Most CPAs recommend caution here because home office deductions for rental management are a higher audit risk area.

What's the difference between active and material participation? Active participation is the lower standard — you make management decisions like setting rents and approving repairs, and you can still hire a property manager. Material participation requires much more substantial involvement and is what's needed for real estate professional status. Most investors with day jobs are active participants, not material participants.

Schedule E is a form, but it's really a mirror. It reflects how well organized your finances have been all year. Investors who dread tax season are usually dealing with the same underlying problem: income and expenses tracked at the account level, not the property level, across a mix of entities that weren't designed to produce clean year-end reports.

That's a solvable problem. It requires accounting software that understands the structure of a real estate portfolio — every property, every entity, every transaction categorized as you go. When your CPA asks for the Schedule E prep work in March, you should be sending a report, not starting a project.

Kestrel RMS is built for exactly this — real estate investors managing multiple properties across multiple entities who want one platform to track every dollar and generate tax-ready reports without the annual scramble. See how it works →

This article is for informational purposes only and does not constitute tax, legal, or financial advice. Consult a qualified CPA or tax professional before making decisions based on this information.

Our real estate proforma is a forward-looking financial model (in Excel) built to help investors understand a property’s projected performance so you can make informed decisions with confidence.

Real estate portfolio management &

accounting software

Your data secured by Plaid.

Copyright 2026 Kestrel, LLC